Inventory: Robust Purchase For The Godfather Of AI")

Justin Sullivan

Nvidia Company (NASDAQ:NVDA), the “godfather” of synthetic intelligence (“AI”) shares, has dropped by about 20% from its latest all-time excessive because the rolling correction ravages the inventory market. Nonetheless, we must always see extra transitory draw back in Nvidia because the selloff continues, and there’s a excessive chance that we’ll have a substantial shopping for alternative quickly.

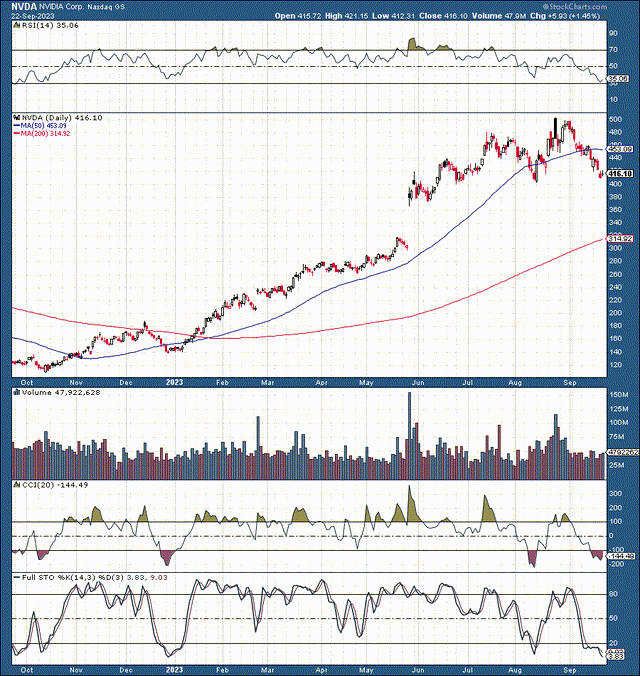

Nvidia: 1-Yr Chart

NVDA (StockCharts.com)

Nvidia may break by way of important assist within the $400-380 vary, resulting in an accelerated selloff into my $370-320 buy-in rage, coinciding with a vital gap-fill across the $320 degree.

Nvidia stays essentially the most profitable AI inventory globally. Nvidia produces essentially the most highly effective GPUs, enabling it to do a lot of the “heavy lifting” within the burgeoning AI discipline. Furthermore, Nvidia’s information middle phase continues to develop quickly and may proceed gaining market share and rising revenues.

Nvidia’s latest earnings bulletins have been wonderful, and it ought to proceed surpassing analysts’ estimates as we advance. Moreover, regardless of Nvidia’s substantial run-up because the bear market backside, its ahead P/E ratio (fiscal 2025) is comparatively low (25 estimate the settlement). Furthermore, Nvidia’s valuation ought to turn into even cheaper as its inventory worth drops within the coming periods. Additionally, we must always proceed seeing income and EPS development outperformance, suggesting that Nvidia’s inventory is cheaper than it appears.

We should always have a rare long-term shopping for alternative as Nvidia’s inventory enters my $370-320 buy-in vary.

Nvidia: “The Godfather” Of AI That Does The Heavy Lifting

“Corporations in each trade are racing to undertake generative AI.” – Jensen Huang, founder and CEO of Nvidia.

Nvidia’s world-leading applied sciences energy the main techniques producers’ servers, enabling firms in any trade to prepared their enterprise for generative AI. Nvidia-powered generative AI may permit a whole bunch of hundreds of corporations to implement functions like clever chatbots, assistants, search and summarization, and extra.

Estimates recommend that Nvidia-powered generative AI cloud could add as much as $4.4 trillion to the worldwide financial system yearly. Generative AI cloud advantages for enterprises embody privateness, alternative, efficiency, information middle scale, decrease value, accelerated storage, “accelerated” networking, speedy deployment, and extra.

Nvidia gives essentially the most superior AI options prepared for enterprises as we speak. Nvidia’s superior AI program gives the “entire package deal.” With Nvidia, organizations get the newest cutting-edge applied sciences. Furthermore, Nvidia gives an entire spectrum of AI fashions and providers, AI platform software program, and the AI supercomputer.

Nvidia gives superior AI providers, software program, and {hardware} options concurrently. Furthermore, Nvidia possesses essentially the most superior GPU applied sciences required to do the “heavy lifting” powering AI. Due to this fact, Nvidia is the “Godfather” of AI and may proceed benefiting because the AI revolution takes off.

Nvidia’s spectacular income development ought to proceed, and the corporate has an exceptionally lengthy development runway as a result of its dominant place in GPU applied sciences and its market-leading place within the information middle phase and AI. Moreover, Nvidia ought to turn into more and more worthwhile, resulting in a a lot greater inventory worth within the coming years.

Greatest Earnings I’ve Seen In Over 20 Years

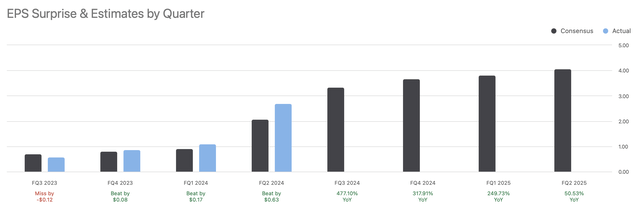

Nvidia’s outcomes communicate for themselves, and its latest earnings outcomes are the very best I’ve seen in my 20-plus years of investing. It began earlier this 12 months when Nvidia reported its blowout fiscal Q1 2024 earnings outcomes. Nvidia crushed the estimated income determine, delivering roughly $7.2 billion vs. the anticipated $6.5 billion. Whereas the ten% income beat was extremely spectacular, Nvidia’s Q2 2024 steering shocked the world, opening my eyes to the large AI alternative in Nvidia’s inventory.

Nvidia guided fiscal Q2 2024 revenues of $11 billion vs. the anticipated $7.11 billion. This outcome was a staggering 55% income improve over the consensus estimate. This steering was on prime of Nvidia’s Q1 file information middle revenues, illustrating its monumental potential in AI.

Quick-forward to fiscal Q2 2024 – Nvidia reported $13.51 billion in revenues vs. the anticipated $11.22 billion estimate. Due to this fact, Nvidia’s Q2 revenues have been 90% above the preliminary estimate, a 102% YoY improve. Moreover, Nvidia reported surging information middle gross sales of $10.32 billion, 29% above estimates. Furthermore, information middle revenues skyrocketed by 171% YoY.

Once more, Nvidia supplied surprising income steering of $16 billion for fiscal Q3 2024, 28% above the $12.5 billion estimate. Nvidia’s stellar outcomes and extraordinary steering illustrate the jaw-dropping demand within the information middle house. Moreover, we should acknowledge Nvidia’s market-leading place in AI. Its information middle gross sales development considerably surpasses its rivals like Superior Micro Gadgets, Inc. (AMD) and Intel (INTC).

As well as, Nvidia permitted a $25 billion buyback program and just lately launched a dividend. Moreover, Nvidia’s profitability is bettering significantly, because it supplied $2.70 in EPS final quarter vs. the anticipated $2.07 per share.

“Nvidia Is Costly” – It is A Fable

EPS vs estimates (Looking for Alpha)

I typically hear that Nvidia is pricey. Sadly, I used this excuse to promote Nvidia earlier than its stellar run-up above $300. Quite the opposite, Nvidia’s earnings development potential illustrates that its inventory is cheap. Subsequent 12 months’s (fiscal 2025) EPS estimates are $16.27, suggesting that Nvidia trades at solely 25 instances ahead earnings right here (consensus estimates). Nonetheless, we noticed Nvidia’s EPS skyrocket just lately, considerably surpassing the consensus estimates. Final quarter, Nvidia beat consensus EPS estimates by over 30%. Due to this fact, there’s a excessive chance that Nvidia will proceed outperforming the consensus estimate figures within the coming quarters.

We may see Nvidia outperform EPS estimates by round 20% in fiscal 2025, implying Nvidia could earn roughly $20 as an alternative of the $16.27 consensus mark. With its inventory round $400, Nvidia trades round 20 instances ahead EPS, exceptionally low cost for a corporation in Nvidia’s dominant, market-leading place and substantial development potential forward. Resulting from Nvidia’s main position in AI, it may proceed exceeding analysts’ estimates, enabling its share worth to go considerably greater within the years forward.

The place Nvidia’s inventory could possibly be in future years:

| Yr (fiscal) | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 |

| Income Bs | $90 | $123 | $154 | $184 | $217 | $250 | $280 |

| Income development | 63% | 37% | 25% | 20% | 18% | 15% | 12% |

| EPS | $20 | $29 | $36 | $44 | $53 | $62 | $70 |

| EPS development | 82% | 44% | 25% | 22% | 20% | 18% | 15% |

| Ahead P/E | 25 | 27 | 28 | 27 | 26 | 25 | 24 |

| Inventory worth | $750 | $972 | $1232 | $1431 | $1612 | $1750 | $1828 |

Supply: The Monetary Prophet

Dangers to Nvidia

Regardless of my bullish projections, Nvidia faces a number of dangers. Whereas Nvidia is the market chief in GPU applied sciences and AI, AMD, Intel, and others are worthy opponents and will take market share from Nvidia as we advance. Additionally, Nvidia’s revenues may develop slower than projected, and its profitability could also be much less outstanding than my expectations venture. It is also believable that Nvidia’s information middle phase demand slows extra considerably than anticipated, resulting in revenues and EPS declines as an alternative of offering regular development within the years forward. We may additionally see a decrease P/E a number of for Nvidia, suggesting its share worth could climb slower than my estimates recommend. Buyers ought to look at these and different dangers earlier than committing capital to an funding in Nvidia’s inventory.