: Analysts Stay Bullish on Generative AI Tailwinds")

A number of tech shares, together with Nvidia (NASDAQ:NVDA), have witnessed a sell-off lately resulting from persistent macro challenges and considerations about elevated rates of interest. Nvidia inventory has declined about 8% over the previous month. Nonetheless, the inventory has rallied by a formidable 191% year-to-date, because of the demand for its superior graphics processing items (GPU) which can be wanted to construct and practice generative synthetic intelligence (AI) fashions. Regardless of macro uncertainty and worries over slowing demand, analysts stay bullish on NVDA inventory and see the pullback as a pretty alternative to construct a long-term place within the main chip big.

Nvidia’s Latest Efficiency

Final month, Nvidia crushed Wall Road’s expectations by reporting a 101% development in its fiscal second-quarter income to $13.51 billion. Additional strong margins and top-line development fueled a 429% bounce in adjusted earnings per share (EPS) to $2.70.

Specifically, the corporate’s Knowledge Heart section generated a 171% income development, backed by a spike in demand for its HGX platform from cloud service suppliers and huge client web corporations. In the course of the Q2 2023 earnings name, CFO Colette Kress referred to as the HGX platform the “engine” of generative AI and huge language fashions (LLMs), which is being deployed by main corporations, together with Amazon’s (NASDAQ:AMZN) Amazon Net Providers, Alphabet’s (NASDAQ:GOOGL, GOOG) Cloud, Meta Platforms (NASDAQ:META), Microsoft (NASDAQ:MSFT) Azure, and Oracle (NYSE:ORCL) Cloud.

Analysts Optimistic on NVDA’s Future Development

Expressing his bullish stance, Morgan Stanley analyst Joseph Moore mentioned on Monday that the latest pullback within the inventory resulting from worries about slowing AI orders for Nvidia from Microsoft has created yet one more alternative to purchase the AI chief. Moore highlighted that an analyst at a data-centric boutique analysis agency famous that Microsoft was decreasing its H100 necessities for 2024, a priority that was heightened by an SEC submitting revealing that NVIDIA has important publicity to a single cloud buyer, which the analyst thinks is “very doubtless Microsoft.”

Moore contended that whereas he can’t touch upon particular 2024 budgets for any single buyer, checks present that demand is properly above provide for NVDA’s H100 chips in lots of areas and with a number of prospects. Additionally, provide chain reviews point out that Microsoft is pushing for extra product than they’re presently getting, which assures that “there isn’t a close to time period air pocket with that buyer.”

Moore reiterated a Purchase score on NVDA inventory with a worth goal of $630, as he expects the corporate to profit from continued AI investments, development in inference platforms, and a B100 GPU product cycle.

Like Moore, Truist analyst William Stein can also be bullish on Nvidia and reaffirmed a Purchase score on the inventory with a worth goal of $668 on Tuesday. Stein referred to as Nvidia and semiconductor firm Monolithic Energy Programs (NASDAQ:MPWR) his favourite concepts. He believes that NVDA’s chips are the “default alternative” for many engineers constructing AI techniques. He additionally thinks that the corporate has sustainable market management in gaming and autonomous driving finish markets.

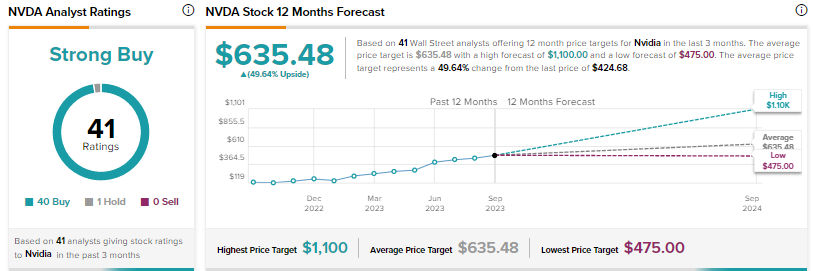

What’s the Prediction for Nvidia Inventory?

With 40 Buys in opposition to only one Maintain advice, Nvidia inventory earns a Sturdy Purchase consensus score on TipRanks. The common worth goal of $635.48 implies about 50% upside potential from present ranges.

Conclusion

Regardless of macroeconomic woes, Wall Road stays bullish on Nvidia and sees continued upside within the inventory even after an exceptional year-to-date rally. Analysts anticipate the demand for Nvidia’s AI chips to spice up its income and earnings over the long run.

Disclosure