Introduction: “Magnificent 7” Are Coming Again To Earth, And So Is Their Chief, Nvidia

Amid a rising rate of interest atmosphere, Nvidia Company (NASDAQ:NVDA) and its huge tech friends have served as a really worthwhile hiding spot for traders, in an obvious “flight-to-quality” commerce. Whereas the “Magnificent 7” shares are nonetheless up considerably in 2023, these beforehand high-flying huge tech shares have been taking successful ever for the reason that market fashioned a neighborhood high in mid-July, with the promoting strain selecting up over the previous couple of classes.

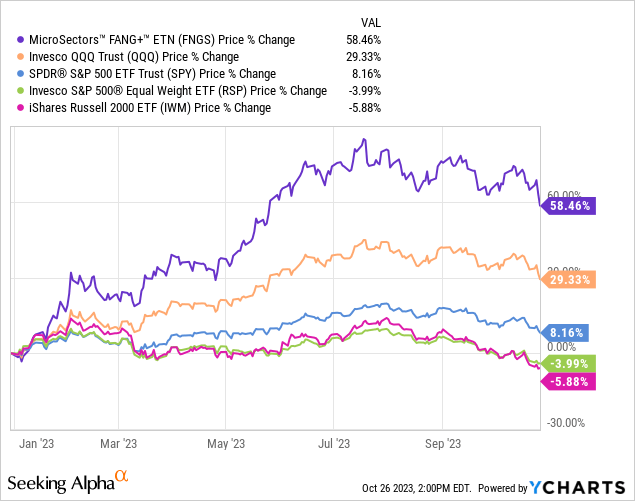

Information by YCharts

Main U.S. fairness indices (SPY, QQQ) have reconnected with key technical ranges such because the 200-DMA [or are close to doing so]with the fast run-up in long-duration treasury yields lastly taking some wind out of massive tech sails. Nevertheless, I feel the stock-bond dynamic has shifted or is shifting proper now, with traders lastly promoting shares to purchase bonds in an actual “flight-to-safety” commerce. The financial system is doubtlessly headed right into a recessionary or stagflationary atmosphere, and heightened geopolitical dangers pose the specter of a black swan occasion for the markets.

In current months, I’ve issued a number of warnings about unwarranted valuation premiums within the huge tech area (particularly in leaders – Apple (AAPL) and Microsoft (MSFT) – damaging fairness threat premiums) and outlined the top-heavy nature of this market as a major threat to main fairness indices:

An enormous chunk of this 12 months’s rally in tech has been attributed to breakthroughs in Generative AI (argued by bulls) or the hype round it (by bears). Whereas we now have seen tons of product bulletins and releases from quite a lot of firms, monetization of Generative AI know-how stays an unsolved thriller [outside of Nvidia, which is the “picks & shovels” provider of this AI race].

After releasing their Q3 stories earlier this week, main AI shares akin to Microsoft, Alphabet/Google (GOOGL), and Meta Platforms (META) have not fared all that effectively, with traders seemingly dejected by a transparent lack of progress on the monetization of Gen AI services which are consuming up billions of {dollars} in CAPEX funding.

Now, as a “picks & shovels” supplier using the red-hot generative AI theme, Nvidia is more likely to ship one other blowout quarter subsequent month and Nvidia’s AI GPU (and now CPU) chips are projected to promote like hotcakes for the subsequent few years [despite the U.S. banning exports of advanced AI chips to China].

If there’s any actual, confirmed beneficiary of the generative AI development, it’s Nvidia. And but, Nvidia’s inventory has misplaced appreciable floor in current classes, together with its huge tech friends. From a basic perspective, I feel Nvidia will proceed to carry out effectively in upcoming quarters since its main clients (cloud hyperscalers) stay dedicated to their aggressive CAPEX spending plans within the hunt for AI dominance.

In my current article “Nvidia: The Magnificent One Delivers On Its AI Promise,” I shared the next stance on NVDA inventory:

With Nvidia Company inventory as soon as once more breaking out to new all-time highs within the after-hours session, I see no resistance for the inventory, i.e., the sky is the restrict for this AI chief. Buyers and analysts have been chasing NVDA larger and better in an effort to stake their declare within the “AI rush”, and as of now, Nvidia stays the obvious “picks and shovels” play out there.

WeBull Desktop

Technically, Nvidia’s inventory is considerably overbought; nevertheless, we all know that it may possibly keep in overbought territory for lengthy durations of time, and momentum can carry NVDA inventory to unimaginable ranges. Given Nvidia’s strong monetary efficiency and administration’s optimistic outlook, I do not suppose traders (institutional or retail) are going to be in any hurry to race towards the exit doorways right here.

I’ll sound like a damaged report however I’ll say this once more –

Nvidia Company is a good firm with market-leading merchandise and arguably the perfect CEO within the semiconductor trade. Nevertheless, the value we’re being requested to pay for Nvidia (~$1.2T) is just too steep, for my part. In a zero-interest price world, traders can afford to be valuation agnostic; nevertheless, we’re not working in such an atmosphere, with the FED nonetheless pulling liquidity out of monetary markets and a financial institution credit score tightening cycle in impact after a number of financial institution failures.

A valuation compression nonetheless seems inevitable for Nvidia, and whereas the long-term threat/reward on provide is wanting respectable after Q2 2023, the inventory affords little to no margin of security to long-term traders.

Within the case of Nvidia, the AI hype is actual, and I’ve been incorrect on the inventory up to now. That mentioned, regardless of operating the danger of lacking out on additional positive factors in NVDA inventory, I select to stay on the sidelines on this counter. Whereas Nvidia is delivering distinctive monetary efficiency proper now, I proceed to imagine that the present price ticket leaves little to no margin of security for a long-term investor. Given the shortage of income visibility going into a possible financial recession (onerous touchdown), I’m “Impartial” on Nvidia Company inventory at these elevated ranges.

Key Takeaway: I proceed to price Nvidia Company inventory “Keep away from/Impartial/Maintain” at $500.

Since then, Nvidia has dropped by practically 20% or $100 per share, and it’s now buying and selling very near our honest worth estimate of $390 (shared within the be aware linked above). In gentle of NVDA’s value decline, Nvidia’s 5-year anticipated CAGR has moved as much as ~20%, rendering the inventory a “Purchase.” Nevertheless, as I shared in my earlier be aware –

I feel our up to date mannequin for Nvidia could be very beneficiant, and lofty assumptions go away little margin of security.

Supply: Nvidia: The Magnificent One Delivers On Its AI Promise.

As of right this moment, I stand by our mannequin assumptions, honest worth estimate, and projected returns. Nevertheless, given the fast run-up in long-duration bonds and heightened geopolitical dangers, I see a better risk of a tough touchdown within the financial system. And in that situation, our beneficiant FCF margin and gross sales progress assumptions can show to be too aggressive. Earlier than updating our mannequin once more, I wish to overview the Q3 earnings report (anticipated November twenty first) and be taught in regards to the enterprise’ trajectory from Nvidia’s administration in the course of the convention name.

So, is Nvidia a purchase, promote, or maintain at present ranges?

From a basic perspective, I see no materials weak point in Nvidia for the foreseeable future given the optimistic read-through from cloud hyperscalers (Microsoft and Alphabet), Meta Platforms, and Tesla (TSLA). The valuation is topic to debate, and I’m not completely assured in our long-term progress and margin projections because of the elevated chance of the financial system slipping right into a recession in some unspecified time in the future throughout the subsequent 12 months. Therefore, I wish to depend upon technical evaluation on this explicit case to assist us make an knowledgeable funding determination.

Nvidia’s Tryst With Troublesome Technicals

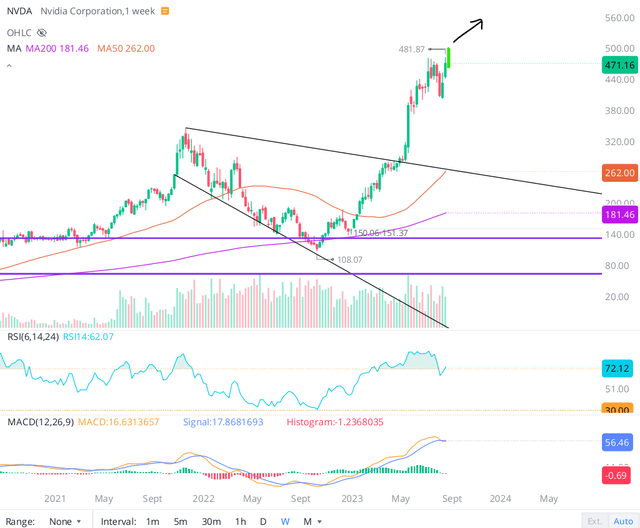

Again at $500 per share, I refused to chase NVDA inventory regardless of mentioning that technically, the sky is the restrict for Nvidia with no resistance at an all-time excessive. Nevertheless, on the again of a ~20% decline, Nvidia Company inventory is now in a technical correction and presently sits at a make-or-break degree at ~$400 per share, with numerous air beneath this psychological degree.

On the weekly chart, Nvidia seems to be forming a rounding high. With RSI and MACD indicators rolling over, Nvidia breaking the $400 degree might set off a pointy selloff as a result of there’s little to no help on the chart. As you possibly can see under, Nvidia went up from ~$250-300 to ~$400-500 in a straight line, and in technical evaluation, we are inclined to see such vertical strikes get re-traced.

WeBull Desktop

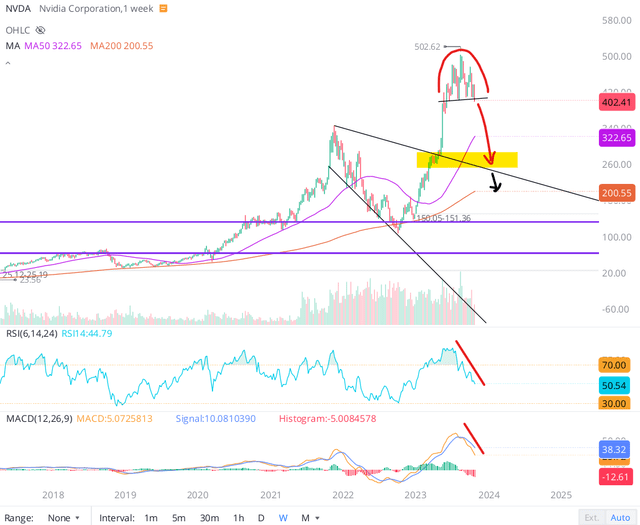

Zooming in utilizing the each day chart, we are able to observe the formation of a bearish “Head And Shoulders” sample in NVDA inventory with the neckline at ~$400-410. Whereas we have not damaged the neckline but, NVDA is poking underneath this key trendline, and a breakdown right here appears inevitable given the technical breakdowns we’re seeing in different huge tech shares and main fairness indices.

WeBull Desktop

If NVDA inventory breaks the $400 degree and we see follow-through promoting within the subsequent few classes, I might view it as a affirmation of the “H&S” sample. A bearish “H&S” sample that I highlighted for QQQ is already taking part in out, and I would not be stunned if Nvidia joined the bear parade right here. Whereas Nvidia might discover some help on the 200-DMA degree [$350]the measured goal of the “H&S” sample is $300, which additionally occurs to be the technical hole fill degree for Nvidia inventory.

Concluding Ideas

In gentle of a -20% decline since my final replace on Nvidia, the long-term threat/reward for NVDA inventory has improved considerably, with the inventory shifting nearer to my honest worth estimate of $390 and the 5-year anticipated return rising to almost 20%. As a picks & shovels play, Nvidia ought to proceed to profit from the continuing AI CAPEX spending bonanza from different huge tech firms. Therefore, I feel Nvidia’s monetary efficiency will proceed to stay robust, not less than within the close to time period.

That mentioned, the wild run-up in long-duration treasury yields has elevated the chance of a tough touchdown, which might negatively affect the demand for Nvidia’s AI chips. Additionally, the U.S. ban on the export of AI chips to China poses a contemporary problem for our long-term progress projections for Nvidia. Given our valuation mannequin for Nvidia is kind of beneficiant, I nonetheless do not suppose we now have a margin of security to deploy contemporary capital into Nvidia.

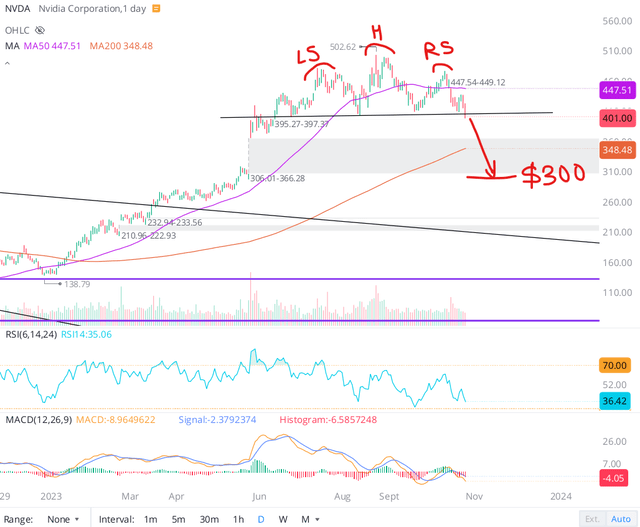

Technically, Nvidia’s inventory is buying and selling at a make-or-break degree. A breakdown right here might ship the inventory right into a tailspin down by ~25% to $300 per share. Regardless of robust beats from its huge tech friends for Q3, Nvidia and the “Magnificent 7” names are experiencing elevated promoting strain in current classes, with main market indices breaching key technical ranges.

current market motion, I imagine a “flight-to-safety” commerce into long-duration treasury bonds [real safe haven] is seemingly underway, and much more cash might come out of (beforehand high-flying) huge tech shares [perceived safe havens] within the subsequent few weeks and months.

Given the heightened macroeconomic, geopolitical, and technical headwinds, I can not justify shopping for Nvidia at present ranges. If we do see a breakdown of the $400 degree (affirmation of the “H&S” sample), then I feel NVDA inventory will slide right down to $250-350 vary in a jiffy.

For daring traders keen to climate volatility, Nvidia Company inventory could possibly be a good wager proper right here. Nevertheless, contemplating the near-to-medium time period threat/reward, I shall be staying on the sidelines for now, but when NVDA will get right down to $250-300, then rely on me to be a purchaser.

Key Takeaway: I price Nvidia “Impartial/Maintain” within the low ~$400s.

Thanks for studying, and comfortable investing! When you have any questions, ideas, and/or issues, please be at liberty to share them within the feedback part under.

(NVDA)")