Simply 10 days from now, chips ‘n’ AI star Nvidia (NASDAQ:NVDA) is scheduled to report its newest batch of monetary outcomes. Analysts are exuberant over the information Nvidia may report, forecasting as a lot as 5x development in quarterly revenue, from $0.58 per share a 12 months in the past, to $3.16 per share right now. And but, one analyst specifically deviated from the herd to publish a think-piece that’s much less obsessive about the {dollars} and cents that Nvidia will report for its fiscal Q3 2024 later this month, and extra involved with how Nvidia might earn much more cash sooner or later.

Titling his report an abbreviation-heavy “NVDA: DGX Cloud + AI Enterprise (Software program) Monetization = $30/Sh+ Worth Creation Forward?”, Wells Fargo’s Aaron Rakers, a 5-star analyst rated within the prime 1% of Wall Avenue’s inventory professionals, mused about Nvidia’s capacity to monetize its software program to energy the “subsequent section” of its development story. And particularly, he questioned aloud whether or not Nvidia may, over simply the following few years, construct a software-only enterprise that would generate $4 billion to $5 billion in annual income — and earn $2 billion to $3 billion in working revenue from it.

If he’s proper in his predictions, this may indicate wherever from 50% to 60% working revenue margins from this new enterprise section — each on prime of and much superior to the already strong 33% working margin than Nvidia will get from promoting laptop chips.

As Raker observes, software program is a comparatively new enterprise for chipmaker Nvidia, and this “subsequent section” within the firm’s development story is at present “in very early innings” — however he expects the potential to grow to be “more and more seen” and in very brief order.

Because the report’s title suggests, Raker thinks the brand new software program will embrace (1) AI Enterprise Software program, in addition to software program to run cloud-based AI supercomputing companies, (2) Omniverse Enterprise software program (so digital actuality), and in addition (3) NVIDIA DRIVE software program utilized in electrical and autonomous automobiles, specifically EVs from Mercedes-Benz and Jaguar Land Rover. Based on Raker, the inflection level at which these three income streams grow to be seen (and materials) to traders might arrive as early as 2025. However already in 2023 we might see software program revenues prime a fairly materials $1 billion, and scale shortly thereafter.

Traders are more likely to acquire perception into this improvement when Nvidia stories its Q3 earnings on November 21, together with steering for the rest of fiscal 2024. If the quantity “$1 billion” pops up as Nvidia turns the dialogue to software program, that will probably be a reasonably large clue that Raker is onto one thing right here.

It’s price stating that Raker bases this suggestion on estimates of future Nvidia earnings which can be truly conservative relative to consensus estimates on Wall Avenue — 3% under estimates for fiscal 2024 earnings (at $10.95 per share) and 20% under estimates for fiscal 2025 earnings ($17.50 per share). If he’s proper about these numbers usually, however incorrect on the contribution that software program gross sales will make to Nvidia’s earnings — then everybody else on Wall Avenue goes to end up wanting very incorrect certainly.

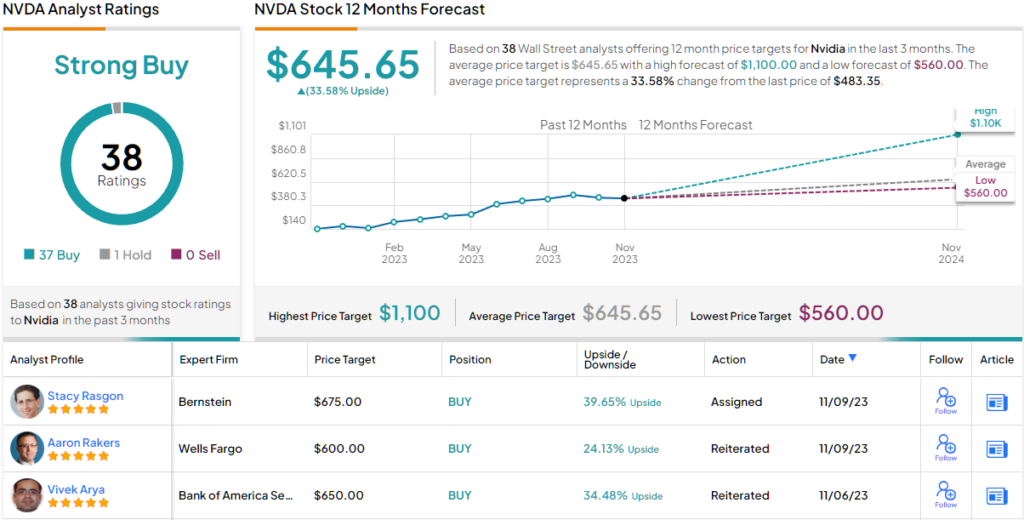

Within the meantime, Raker is ranking Nvidia inventory an Chubby (i.e. Purchase) with a $600 value goal, which means a 24% upside from present ranges. (See Raker’s observe document)

Nearly nobody is arguing with that tackle Wall Avenue. The inventory’s Robust Purchase consensus ranking relies on 37 Buys and a single Maintain. The forecast requires one-year good points of ~34%, contemplating the typical goal stands at $645.65. (See NVDA inventory forecast)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analyst. The content material is meant for use for informational functions solely. It is vitally vital to do your personal evaluation earlier than making any funding.