")

David Becker

Funding thesis

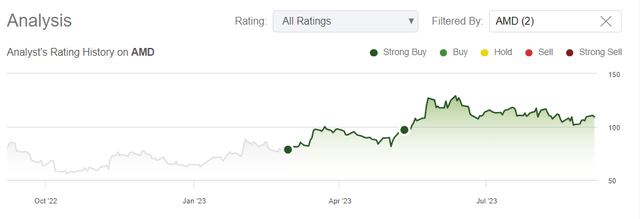

My first two calls about Superior Micro Gadgets, Inc. (NASDAQ:AMD) inventory labored effectively, outperforming the broader market because the articles went stay.

Looking for Alpha

The inventory considerably underperformed Nvidia (NVDA) this 12 months, however that implies that the valuation continues to be very engaging regardless of a year-to-date rally. The primary half of 2023 was difficult for the corporate as a result of weak PC market, however a number of indicators inform me that the worst is within the rearview window. The corporate’s stable profitability and fortress stability sheet enabled it to proceed investing closely in innovation even in the course of the double-digit income decline. The corporate’s investments had been aimed on the enchancment of well-known choices in addition to enlargement into the generative synthetic intelligence (“AI”) market, which requires extra highly effective chipsets. The corporate has promising new choices to deal with the new generative AI area and the stable historical past of success offers a excessive stage of conviction that the corporate is ready to reach new ventures as effectively. All in all, I reiterate my “Sturdy purchase” ranking for AMD.

Current developments

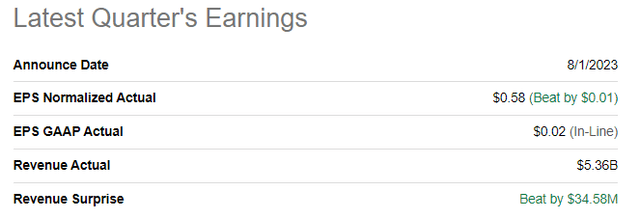

AMD reported its newest quarter’s earnings on August 1, when the corporate topped consensus estimates. Income declined 18% YoY and was flat sequentially.

Looking for Alpha

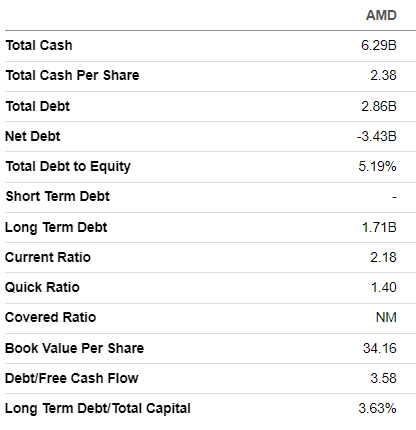

Regardless of a notable income decline within the final two quarters, the quarterly gross margin of 49.5% continues to be removed from its all-time excessive. The working margin was virtually zero in Q2, nevertheless it was principally as a result of elevated R&D to income ratio and never as a result of spike in SG&A. Regardless of experiencing headwinds, the corporate’s fortress stability sheet allows the corporate to proceed reinvesting a few quarter of its gross sales in innovation. I like the corporate’s robust and constant dedication to innovation, even within the present unsure surroundings.

Looking for Alpha

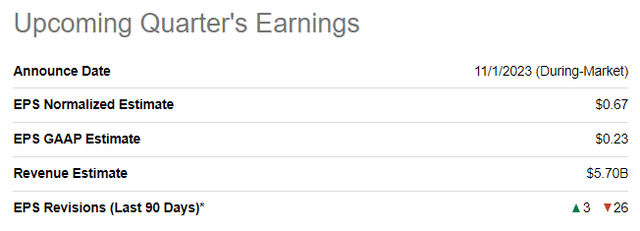

The upcoming quarter’s earnings are scheduled for launch on November 1. Quarterly income of $5.7 billion signifies a 2.3% YoY progress, which is according to the corporate’s expectations shared in the course of the Q1 2023 earnings name that income will rebound within the second half of 2023. What can be essential to me is that the adjusted EPS is predicted to return to $0.67, which might be flat YoY.

Looking for Alpha

I like that the corporate continues investing closely in innovation even amid the present difficult surroundings. For me, this means agency confidence in favorable secular traits for AMD. A wealthy monitor file of success means that if the administration didn’t see a chance to construct long-term worth, it could have minimize on R&D spending as an alternative. Certainly, the quickly growing penetration of AI-powered options for each companies and people requires far more {hardware} and computing energy. AMD is well-positioned to learn from the favorable AI secular development by providing the market a complete set of {hardware}. The corporate not too long ago launched its new generative AI accelerator. Given AMD’s robust monitor file of profitable product launches, this accelerator can change into a stable competitor to Nvidia’s choices which presently dominate the generative AI area.

AMD’s newest earnings name presentation

The near-term outlook additionally appears optimistic to me, regardless of the general difficult surroundings. The primary half’s income of AMD suffered considerably from a weak PC market, which the corporate believes has bottomed in Q1. Lenovo, the world’s largest PC maker, additionally shared the opinion not too long ago, that the worst is over for the PC market. It’s also essential to emphasise that in the course of the newest Deutsche Financial institution Know-how Convention, Jean Hu, the CFO shared his imaginative and prescient relating to potential tailwinds for the PC trade in 2024:

Second half seasonally usually, PC is healthier. And subsequent 12 months, you do have a Home windows 10 end-of-life and doubtlessly the AI functions that can assist the refresh cycle. So we’re fairly optimistic concerning the PC and the consumer enterprise, the stock, and the sell-through have been normalized.

To conclude, I consider that the corporate has executed fairly effectively throughout this 12 months’s first-half turmoil, and its substantial investments in R&D throughout this short-term disaster make it now well-positioned to soak up the PC market restoration along with secular traits associated to Generative AI.

Valuation replace

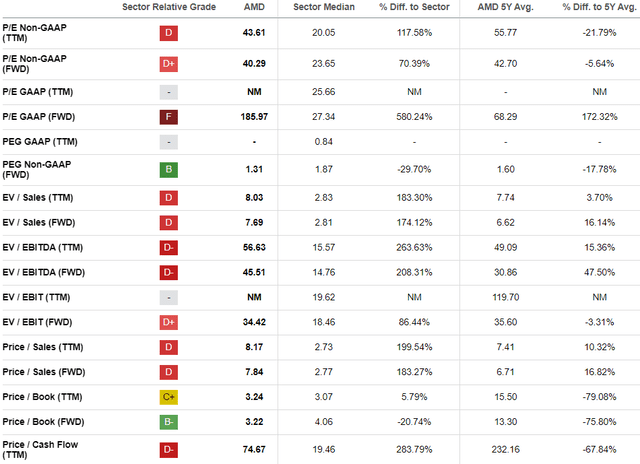

The inventory delivered a large 70% rally year-to-date, considerably outperforming the broader U.S. market and the iShares Semiconductor ETF (SOXX). Looking for Alpha Quant assigns the inventory a median “C-” valuation grade, which means the inventory is roughly pretty valued. From my viewpoint, I believe that comparisons to the sector median and historic averages are blended and don’t give us a transparent image.

Looking for Alpha

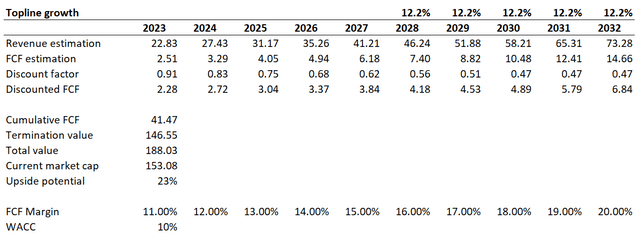

To make it extra clear, I wish to simulate the discounted money circulate [DCF] method. I exploit a ten% WACC for discounting. Eleven p.c is a TTM FCF (free money circulate) ex-SBC (stock-based compensation) margin, which I think about truthful sufficient to make use of for my base 12 months. I count on the FCF margin to broaden by one proportion level yearly because the enterprise scales up additional. I’ve income consensus estimates accessible as much as fiscal 12 months 2027. For the years past, I applied a 12.2% CAGR.

Writer’s calculations

In accordance with my DCF evaluation, the inventory continues to be about 23% undervalued regardless of a large year-to-date rally. It’s also essential to emphasise that the corporate’s $3 billion internet money place positively impacts the truthful worth, however I exclude it from calculations to be extra conservative.

Dangers to think about

The inventory market sentiment has deteriorated notably over a number of current weeks. The explanations are on the floor: the downgrade of the U.S. credit standing, the Fed’s ongoing hawkish rhetoric, and the deteriorating credit score scores with unfavourable shifts in outlook for some main regional banks. All these components don’t favor progress shares, as a result of they in the end result in larger rates of interest, which undermines the discounted values of future money flows. Subsequently, it could be difficult for AMD’s inventory to go up towards its truthful worth within the close to time period. That stated, traders ought to be able to abdomen short-term volatility and be long-term-minded.

The semiconductor trade is likely one of the hottest this 12 months after Nvidia’s inventory worth greater than tripled in 2023 attributable to optimism relating to the doubtless skyrocketing demand because of speedy generative AI adoption. I’ve a agency conviction that NVDA is considerably overvalued, even contemplating its traditionally beneficiant valuations.

That stated, there’s a excessive danger that Nvidia traders may see a considerable inventory worth correction within the close to time period. Since it’s by far the largest semiconductor firm on the earth, from the market cap perspective, traders may begin promoting off smaller names like AMD as effectively. When such a danger exists, I consider that greenback averaging can be the most suitable choice for long-term traders.

Backside line

To conclude, AMD continues to be a “Sturdy purchase.” The inventory may be very attractively valued even after a large year-to-date rally. Nvidia has been dominating the generative AI subject, however I believe that AMD’s new choices are capable of compete with the chief and acquire its market share. Many shreds of proof present that the disaster within the international PC markets has bottomed out and the restoration will begin within the second half of this 12 months. Given the corporate’s constantly robust dedication to innovation even within the two straight difficult quarters makes it well-positioned to learn from the rebound in international PC shipments.