")

William_Potter

NVIDIA Company (NASDAQ:NVDA) has wildly fallen out of favor as among the synthetic intelligence (“AI”) hype wanes. As well as, the U.S. authorities continues to press for chip corporations to not promote superior AI chips to China inflicting potential gross sales disruptions. My funding thesis stays Impartial on the inventory, in search of a further selloff on Nvidia to supply an opportune time to purchase the AI chip firm.

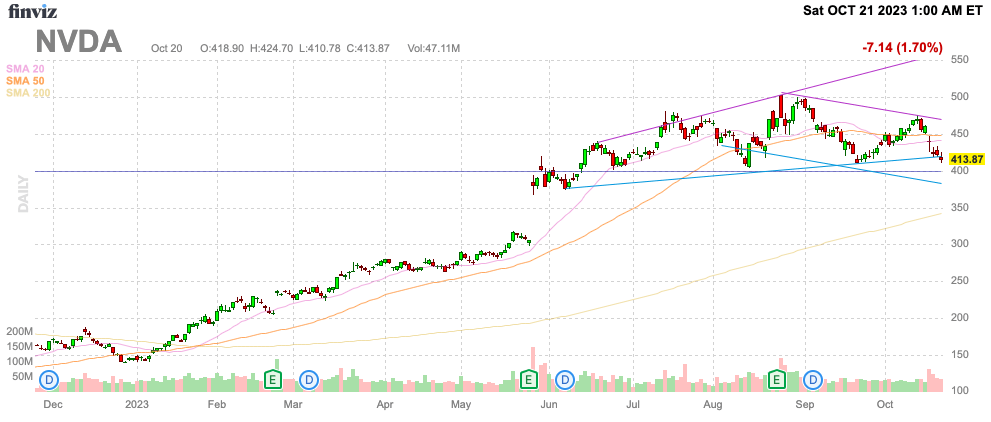

Supply: Finviz

China Danger

The U.S. authorities issued new guidelines curbing the gross sales of AI chips to China. The brand new restrictions from the U.S. Commerce Division immediately goal the A800 and H800 chips modified particularly for the Chinese language market to adjust to prior export controls.

The up to date restrictions apparently permit for superior industrial chips, however the U.S. authorities strikes up restrictions to 40 international locations the place China may use the federal government as an middleman. The information experiences already highlighted how Saudi Arabia and UAE oddly have been massive consumers of the AI GPUs from Nvidia, and huge tech corporations, equivalent to Ali Baba (BABA) and Baidu (BEGINNING), in China apparently ordered $5 billion value of A800 chips.

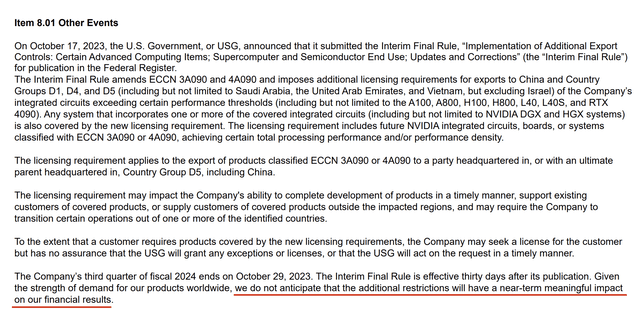

Nvidia claims the brand new China AI chip restrictions have a restricted influence on near-term outcomes. The key implication is that China demand was all pulled ahead to front-run these feared further restrictions.

Supply: Nvidia 8-Okay

KeyBanc Capital Markets analysts bolstered our view of the monetary influence to Nvidia:

We consider this growth probably may have minimal influence [near-term] to NVDA, correctly in a position to backfill with demand from [the rest of the world]

The AI chip firm may be very clear in suggesting the up to date AI chip export guidelines is not going to have a near-term influence. The suggestion is that the ban may have a long-term influence with Nvidia finally struggling to backfill China demand, which represents as much as 25% of revenues.

The corporate just lately guided to FQ3 revenues of $16+ billion after reporting $13.5 billion for FQ2’24. Nvidia solely produced FQ1 revenues of $7.2 billion and the consensus goal for FQ2 was simply $11.1 billion.

The present quarter ends in 10 days, so Nvidia clearly would not face a lot monetary influence on the October quarter now. As a result of chip firm probably pulling ahead China demand and probably transport by way of Saudi Arabia, the corporate may simply have pushed again further demand from international locations not going through restrictions.

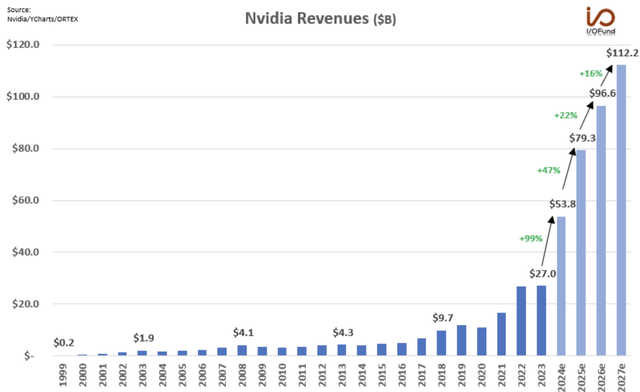

Analysts forecast revenues surging one other 46% to succeed in $78.8 billion in FY25. Primarily based on this chart, analysts are forecasting huge gross sales development with FY27 reaching $112.2 billion, which is ~350% development in these years.

Supply: Beth Kindig – Twitter/X

Oddly Low-cost

Nvidia has fallen all the way down to $414 whereas monetary projections have soared. The inventory truly trades at a really cheap 25.6x FY25 EPS targets.

Supply: Looking for Alpha

The market positively must query how Nvidia nonetheless hits the FY25 EPS goal of $16.48. The AI chip firm requires over 50% earnings development subsequent 12 months to succeed in this quantity. Technically, the quantity would seem close to unimaginable primarily based on the China AI chip ban, however the chip firm probably has a plan on circumventing the export ban.

The inventory truly trades under the ahead P/E a number of again in early 2023 previous to the massive income and EPS guide-up. Nvidia traded at practically 40x ahead EPS estimates when the inventory was buying and selling at $225 and analysts solely forecast FY25 EPS estimates of ~$5.50.

As a result of fears over China AI chip bans and the precarious place of the inventory chart, traders ought to search for Nvidia to shut the hole to just about $300 previous to the massive guide-up in revenues that occurred on the finish of Could. Contemplating the inventory faces a bearish H&S sample, the market negativity, and the precarious place of the AI chip ban, Nvidia is more likely to shut the huge hole on the chart.

In the end, Nvidia is more likely to resolve the China AI chip challenge and ultimately accumulate these huge knowledge heart income alternatives. Such a attainable answer could possibly be China figuring out a knowledge heart utilization plan with an exterior ally in a position to import the AI chips with China allowed to entry cloud computing providers.

The inventory positively trades as if the monetary targets highlighted above might be unimaginable to hit with China export curbs in place. Nvidia would not commerce at half the present development charges and prior P/E a number of if traders have been assured within the consensus targets, although the numbers have not been adjusted down this final week

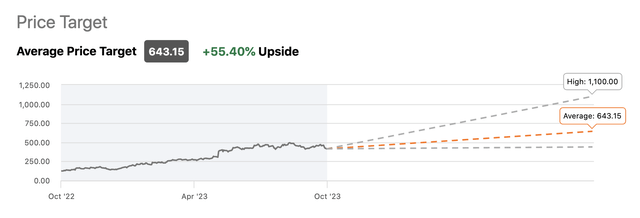

A number of analysts discount targets just lately, equivalent to Citi chopping the value goal $55 to a still-high $575. Regardless, the consensus analyst targets are up at $643 offering over 55% upside to Nvidia now.

Supply: Looking for Alpha

The inventory may positively maintain on the present worth and rally. Traders should be ready for both end result, however the preferrred time to purchase shares for optimum return and decreased danger is to attend for a niche near $300 on most concern.

Takeaway

The important thing investor takeaway is that Nvidia nonetheless seems full-speed forward with insatiable AI chip demand. Nvidia Company inventory has hit a wall attributable to China AI chip curbs, however traders ought to use weak point as a possibility, with China and Nvidia probably discovering an answer earlier than gross sales are materially damage. The inventory is definitely cheaper now and additional weak point may flip Nvidia into a worth inventory.