Up 227% YTD. Extra Upside is Probably")

Nvidia (NASDAQ:NVDA) is a pacesetter within the semiconductor business. Its high-end graphics processing models (GPUs) are wildly standard, fueling its income to staggering ranges. The corporate has since then expanded into high-growth markets equivalent to automotive, knowledge facilities, AI, and extra. Its inventory has seen outstanding good points of 227% year-to-date, overtaking the S&P 500’s (SPX) 13% achieve. The sturdy demand for its GPU chips and its skill to evolve on this complicated area of interest is why I’m bullish on NVDA inventory now. Analysts are bullish as effectively.

Nvidia’s graphic processors are utilized in quite a lot of functions, starting from computer systems to online game consoles. Their strong computing capabilities are important for AI-focused duties, enjoying a pivotal position within the success of OpenAI’s ChatGPT and related AI functions.

Nvidia Shattered Q2 Estimates. The Future Seems to be Vibrant

Nvidia reported an astounding 101% improve in income year-over-year to $13.5 billion for the second quarter ended July 30, 2023. Adjusted earnings per diluted share elevated by a whopping 429% to $2.70, smashing the consensus estimate of $2.08 per share, and Knowledge Middle gross sales grew by 171% on account of elevated demand from cloud service suppliers. In the meantime, its Gaming section income grew by 22% within the quarter.

Additionally, the non-public laptop (PC) market is displaying indicators of restoration, in line with market analysis agency Canalysthat means extra gaming income for Nvidia within the coming quarters.

Owing to the heavy demand for H100 GPUs, Nvidia is working to increase the availability of those GPUs over the subsequent few quarters. Therefore, administration expects income of $16 billion in Q3, pushed by this sturdy demand. If the goal is met, that may replicate a formidable 170% improve over the corresponding quarter a 12 months in the past.

Every chip presently prices between $25,000 and $40,000. If demand stays sturdy, it may imply stable, constant income for the corporate.

In the meantime, analysts predict Q3 income within the vary of $12.2 billion to $19.1 billion, with the consensus coming in at $16 billion. Earnings per share may vary from $2.38 to $3.69, in line with analysts, with the consensus EPS estimate coming in at $3.32. The corporate has beat expectations for the previous three consecutive quarters, and its subsequent earnings launch might be on November 21.

Moreover, Nvidia closed Q2 with a sizeable money steadiness of $16.0 billion and $8.46 billion in long-term debt. Its fast development in earnings ought to permit it to repay the debt shortly. Free money circulate within the quarter stood at $6.3 billion, a drastic soar from $837 million within the prior quarter. This surplus money can be utilized to fund future tasks.

Dangers and Rewards

Nvidia continues to forge partnerships and collaborations to bolster its market presence and income development potential. As an example, lately, it collaborated with Indian conglomerates Reliance Industries Restricted and Tata Group to create AI supercomputers utilizing NVDA’s GH200 Grace Hopper Superchip and DGXTM Cloud know-how.

This collaboration would possibly ensue AI-led transformations within the manufacturing, shopper, industrial, and telecommunications sectors.

Whereas the rewards appear attractive, there are additionally dangers. In response to Reuters, OpenAI would possibly look into creating its personal AI chips to fight the shortage of high-priced AI chips. It might additionally intend to diversify its provider base past Nvidia. Moreover, Microsoft (NASDAQ:MSFT) is planning to launch its first AI chip, “Athena,” subsequent month throughout its annual developer convention for a similar causes, in line with The Info.

With rising competitors within the AI area of interest, solely time will inform how this tech titan will capitalize on this large development whereas sustaining its dominant place within the chip market. For now, Citi analyst Atif Malik is optimistic that Nvidia will be capable to maintain its market share of 90% within the AI GPU marketplace for the subsequent two to 3 years. The analyst charges the inventory a Purchase, with a goal worth of $630.

Additionally, analysts predict that Nvidia’s income will improve by 99.4% in Fiscal 2024 and by 47.5% in Fiscal 2025.

This month, Goldman Sachs (NYSE:GS) included the inventory on its Americas Conviction Record. Due to its aggressive moat and sophisticated AI fashions, the financial institution believes Nvidia will be capable to retain its market dominance.

Nvidia trades at 29 instances ahead earnings. Its third-quarter outcomes and analyst forecasts for future quarters will decide whether or not this valuation is justified.

Is NVDA Inventory a Purchase, In response to Analysts?

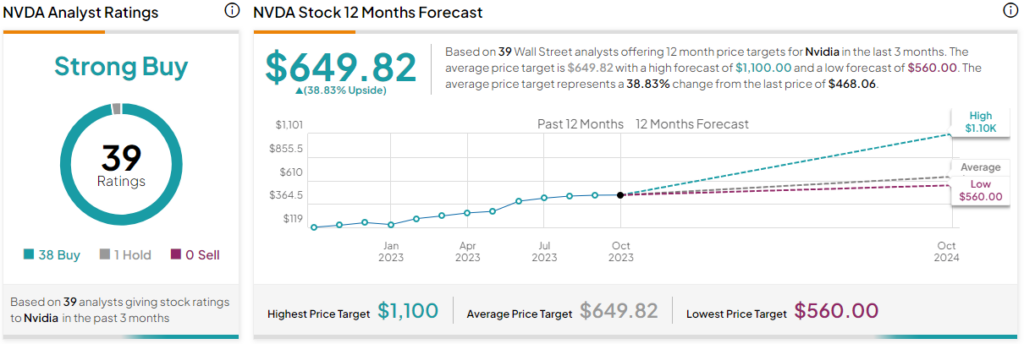

Turning to Wall Avenue, TipRanks charges NVDA as a Sturdy Purchase, with 38 Buys, one Maintain, and no Promote rankings assigned previously three months. The common NVDA inventory worth goal of $649.82 implies 38.8% upside potential. The very best worth goal for the inventory stands at $1,100, whereas the bottom goal worth is $560.

The Takeaway

Nvidia’s income has elevated from $4.3 billion in Fiscal 2013 to an excellent $27.0 billion in Fiscal 2023, reflecting the magnitude of its development. AI, in line with consultants, is simply getting began. Between 2023 and 2030, the worldwide AI market may develop at a compound annual development fee of 36.8%, reaching $1.345 trillion.

Nvidia’s strong market place, numerous product portfolio, and ongoing innovation in AI applied sciences could assist the corporate preserve and even improve income within the coming years. Due to this fact, I’m not shocked as to why Wall Avenue is so bullish on the inventory.

Disclosure