This development is primarily pushed by the demand from the smartphone restore market, the marketplace for second-hand smartphones, and the discharge of latest smartphone fashions. Waiting for 2024, TrendForce anticipates that the supply-demand dynamics of the smartphone market will return to a standard cycle. Consequently, there might be a drop in demand for second-hand gadgets and system restore. TrendForce forecasts that shipments of smartphone panels will quantity to round 1.82 billion items in 2024, reflecting a YoY decline of 9%.

Relating to shipments of smartphone panels from particular person panel makers, the decline in demand for LCD panels is a shared situation for a few of them. Presently, BOE firmly holds the highest place in world smartphone panel shipments, with an estimated cargo of round 560 million items for 2023. Nonetheless, in 2024, BOE is predicted to be impacted by the weakening demand for LCD panels, leading to a projected YoY drop of seven.2% to round 520 million items. Following BOE is SDC in second place. Because of the decline in demand for inflexible AMOLED panels, SDC’s shipments for 2023 are forecasted round 350 million pierces. As for 2024, SDC’s cargo figures are anticipated to stay comparatively on par with the determine 2023 as its efficiency is predicted to be sustained by the demand associated to Samsung’s and Apple’s gadgets. Tianma is estimated to ship round 175 million items of smartphone panels in 2023, securing the corporate’s third-place place. As Tianma expands collaborations with varied manufacturers, there’s a likelihood that its shipments may see a marginal YoY enhance of 5.2% for 2024, totaling about 190 million items.

Innolux is ranked in fourth place in shipments at about 140 million items for 2023 and is projected at about 125 million items for 2024 beneath a YoY discount of 11.2% as a result of shrinking demand from the LCD market. HKC, ranked at fifth place, is estimated at a cargo quantity of 170 million items for 2023 attributed to its price benefit from the G8.6 manufacturing traces, and is projected to develop to 180 million items in shipments for 2024 at a YoY development of 4.2%. TrendForce commented that SDC is the only maker among the many prime 5 gamers that’s deteriorating in shipments throughout 2023 as a result of declining demand for inflexible AMOLED panels, that means that inflexible AMOLED panels made by South Korean makers are progressively subsiding in market shares, after the initiation of mass manufacturing on versatile AMOLED panels by Chinese language makers, on account of inadequate price competitiveness.

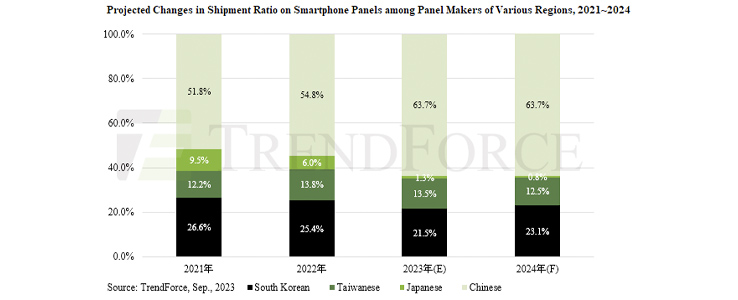

As for the cargo ratio amongst panel makers by area, Taiwanese makers are in a position to maintain onto their proportion because of the help from a-Si LCD, whereas Japanese makers are dropping in shipments attributable to their expeditious exit from the smartphone market. South Korean makers are maintained at 23-25% of shipments attributable to their know-how of versatile AMOLED panels and the corresponding adoption by high-end smartphones. Chinese language makers have ascended from 54.8% (2022) to 63.7% (2023) in total shipments of smartphone panels, which showcases their continued significance within the total smartphone provide chain.

For extra info go to TrendForce.