Unveils New MacBook Professional Forward of This fall Earnings")

Apple (NASDAQ:AAPL), at its “Scary Quick” occasion on October 30, unveiled a brand new MacBook Professional line-up that includes the brand new M3 chips, together with M3, M3 Professional, and M3 Max. The brand new MacBook Professional incorporates a next-gen GPU (Graphics Processing Unit) structure and a sooner CPU (Central Processing Unit), which boosts its capabilities. The launch got here forward of its This fall earnings outcomes scheduled for Thursday, November 2.

Together with MacBook Professional fashions, the corporate additionally launched a brand new 24” iMac.

Following the launch, Goldman Sachs analyst Mike Ng stated that Apple’s “refreshed Mac portfolio” will strengthen its aggressive positioning and allow the corporate to capitalize on the restoration within the PC trade.

Whether or not the brand new Mac portfolio will drive Apple’s high line stays a wait-and-watch story. In the meantime, let’s take a look at analysts’ This fall expectations.

Apple’s – This fall Expectations

Wall Road expects Apple to put up income of $89.30 billion in This fall, which displays a slight decline from the prior-year quarter’s income of $90.15 billion. The anticipated year-over-year decline displays weak point in {hardware} gross sales. It’s price highlighting that iPhone income fell 2% within the June quarter. Additional, Mac and iPad gross sales had been down by 7% and 20%, respectively.

Barclays analyst Tim Lengthy expects the softness in {hardware} gross sales to proceed in This fall. The analyst lowered the worth goal on AAPL inventory to $166 from $167 and stored a Maintain suggestion on October 30. Nonetheless, Lengthy believes that the energy within the Providers section will assist offset the weak point in {hardware} revenues.

Echoing comparable sentiments, KeyBanc analyst Brandon Nispel downgraded Apple inventory to Maintain on October 30. Nispel is extra involved concerning the corporate’s Q1 steerage and expects {hardware} gross sales to say no.

Whereas Apple’s high line might face challenges, its backside line is predicted to indicate an enchancment on a year-over-year foundation. Analysts count on Apple to put up earnings of $1.39 in This fall, which compares favorably to the EPS of $1.29 within the prior-year quarter.

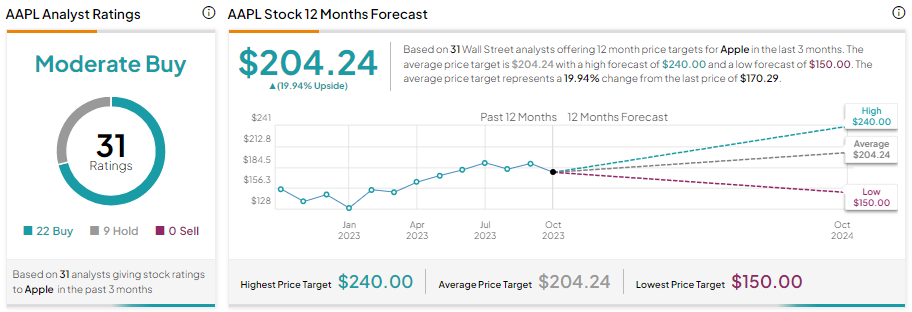

Is Apple a Purchase, Maintain, or Promote?

Wall Road analysts are cautiously optimistic about Apple inventory as a result of short-term headwinds concerning {hardware} gross sales. With 22 Buys and 9 Holds, Apple inventory sports activities a Average Purchase consensus ranking.

Additional, the common AAPL inventory value goal of $204.24 implies 19.94% upside potential from present ranges.

Disclosure